“Captain Bermudez!”

August 26, 2007“Engine Failure”

June 14, 2008OK so here is a quick follow-up for you! People have been asking about the Vette mods and the Lancair repairs, so here we go!

Corvette:

I had Mike Bruce replace the Jedi-Knight-On-Cocaine cam with a ‘Ferrari-like’ cam. This new cam is advanced enough that the engine lopes and gurgles and surges a bit at idle, like an energetic horse that WANTS to run, but is not so rough as to be uncomfortable. At VERY low speed it surges and kicks a bit, but is smooth by the time you get to a mere 1,500 rpm… about 30 mph in third or fourth gear. Then, as you get on it, it becomes a nice loud, aggressive roar as you are pinned back in the seat from tire-spinning torque all the way through first and second gear. In third gear, the car catches a quick tire squeal on a fast shift, but is in little danger of spinning the tires after that on all but the coldest days, on which it can still spin the tires in third.

The sound at full power is just stunning: rrraaaaHHHHHHHHRRRRRRRRRR!!!!!!!!!! as the big, aggressively-cammed engine roars to 7,000 rpm.

The Corvette is 400 hp stock, but now running about 530 hp now according to the dyno.

Remember, these cam and head are about as aggressive as what you find on a Ferrari, but those cars have 3.6 or 4.3 liter engines… this is 6.0 liters.

Really it is just perfect: Just aggressive enough to be fun and have some attitude at very low speed, and wonderfully tuned to give a very strong performance up at high RPM.

I took it on the track (Carolina Motor Parkway, an F-1 track with 18 turns taken between 40 and 110 mph) against Ferraris, Porsches, and other Corvettes.

It was not a race, but a pure demonstration of what that car can do. There was NO-ONE that could stay with it… with the wide, not-heavy chassis of the -07 Corvette, nice large tires with plenty of traction, Z-51 suspension (an option I chose), lower-ratio rear-end (effectively lowering all the gear ratios for tighter low-end gearing, like a Ferrari), traction control (to keep the tires from spinning) stability control (to keep the car from spinning out in the turns) and the extra 33% power from the engine mods, my car was simply a giant red manta-ray in everyone’s rear-view mirror that quickly gobbled them up. I think I passed every car in my group (Ferraris, Porches, Corvettes with intermediate drivers). The Vette was just un-stoppable.

I let a few professional racers drive it and they came stumbling out after a few laps with big silly grins on their faces… they could never imagine that such a pretty, luxurious, COMFORTABLE car could ROAR so smoothly and strongly to 100 in about 7 or 8 seconds. The sound is just so mellow and smooth and strong that it is just a pleasure to listen to, lap after lap after lap. When I let ohers drive, the really good racers would make their gear selections to hold the engine at 75% of redline all the way around the track, always with the perfect gear selection to keep the engine at maximum horsepower, but still making every shift SMOOTH. The better and faster the driver, the SMOOTHER the ride! (MY driving, needless to say, was NOT at a professional level… I wrestled around the track with plenty of neck-snapping shifts, acceleration, braking, and skidding… still holding all the competition at bay with brute power and engineering finess of this car, but the pros were FASTER by driving SMOOTHER).

Below are a few pix me and some friends got on Christmas day… no traffic! Zoom-Zoom! There’s no potoshop here… the picture just turned out that way!

Lancair:

OK they are still working to repair the Lancair, and say it will be ready in a few weeks (they have finally got all the protocols in place, and just doing the work now).

I do NOT carry hull insurance on the plane, so I will be paying the repair bill out of pocket.

Am I foolish for not carrying hull insurance on the plane?

Let’s find out.

I called AVEMCO and got a quote on insuring both the SR-22 (which I no longer have, but I wanted to see what the rate WOULD HAVE BEEN had I insured it) and the Columbia. The bill? $10,000/year (same quote for both planes).

Hull insurance on the Cirrus and Lancair would each be $10,000/year, and I owned the Cirrus for 4 years, Lancair for 1. (so far).

That’s $50,000 I have NOT paid in premiums, but would have paid, had I had hull insurance.

Wait. How much have I SAVED by NOT having insurance? I get 15% in the stock market (agressive-growth international and domestic mutual funds). Look at my first adventure: December of 2003, when I got my Cirrus. Let’s do the math together, dropping $10,000/year into the market from that point, at 15% per year. This is simply dumping our annual hull insurance on a Cirrus or Lancair into the stock market, which is EXACTLY what I have actually done… this is not hypothetical, this is what I really did:

2003: $10,000 into the market that I WOULD have spent in hull insurance for the SR-22

2004: at 15% return, it’s now worth $11,500 plus another $10,000 premiums this year into the market, total $21,500

2005: at 15% return, it’s now worth $24,700 plus another $10,000 premiums this year into the market, total $34,700

2006: at 15% return, it’s now worth $39,900 plus another $10,000 premiums this year into the market, total $49,900

2007: at 15% return, it’s now worth $57,400 plus another $10,000 premiums this year into the market, total $67,400

SO, by NOT buying insurance, I am $67,400 RICHER than I would be if I had bought the insurance. That’s $50,000 in premiums I never paid, and $17,4000 I made in the market by investing it instead. SO I am now $67,400 richer for NOT having bought insurance.

Now, you wanna hear the estimate on the repair?

$15,000.

If the insurance companies had their way, I would have paid them $50,000 in premiums, and deprived myself of $17,400 in investment-income to get $15,000 back. If ever anyone could be said to sell you a nickel for a dime, it is the insurance companies. They do this like no other industry except the gambling industry, which is equally adept at knowing the odds, and being sure to charge MORE than the game is really worth.

So, how smart am I to NOT have insurance? It STUNS me that some people are amazed that I carry no insurance. Simply stuns me.

One of my customers runs an air-freight business. He runs a fleet of about THIRTY Aero-Commanders flying all over the country in the middle of the night. (Their pilots train on X-Plane). He’s been in the biz for about 30 years and lost TWO airplanes in THIRTY years (both BEFORE they started training on X-Plane). He never carried insurance. He paid for TWO planes being lost over THIRTY years. Then the government FORCED him to buy insurance. He had NO choice. The insurance rate? IT WAS EQUAL TO THE COST OF ONE AERO-COMMANDER EVERY SINGLE YEAR. His insurance rates were FIFTEEN TIMES HIGHER THAN HIS ACTUAL LOSS RATE… and that is based on flying a large FLEET of planes for a third of a LIFETIME… PLENTY of time for the law of averages to become clear. He was FORCED to pay the insurance company for a new airplane every single year… though he only actually lost one once every fifteen years.

Everybody reading this: Add up all the insurance premiums you have paid in your life, and the claims you have been paid in return. How’s it looking?

As I was out at the airport overseeing the maintenance on my plane and shooting the breeze with someone there, he nodded to a twin-engine airplane in the hangar right next to my under-repair Lancair. The twin was somewhat-modified and in perfect condition. (new instruments, leather interior, yadda yadda yadda). “You know how much MONEY the owner of that plane makes?” he asked. “About THREE MILLION DOLLARS PER DAY“. Again, that’s $3,000,000 per DAY.

“HOW?!?!?!” I asked, stunned, once I picked my jaw up out of my lap.

The answer: “He runs a big insurance company”.

You don’t believe me? It only takes 110,000 customers at $10,000/year to make that money… and that’s neglecting the investment returns he makes from the proceeds of investing the money. With the market returns he makes by investing your money, he actually needs LESS than 110,000 customers to make his $3,000,000 per DAY.

What if an insurance company DOUBLES your rates? Will you still carry the insurance if you HAVE the money to pay them? What will you do to evaluate whether the payout back to you is worth the premiums you pay? If the worst-case covered loss you could face (your house burning down, for example) is $200,000, and the chance of it happening is 1 in 1000, then an insurance against that risk is worth $200,000 / 1000, or $200… do you think that’s what your premium will be? Have you done the math to find out for YOUR premiums?

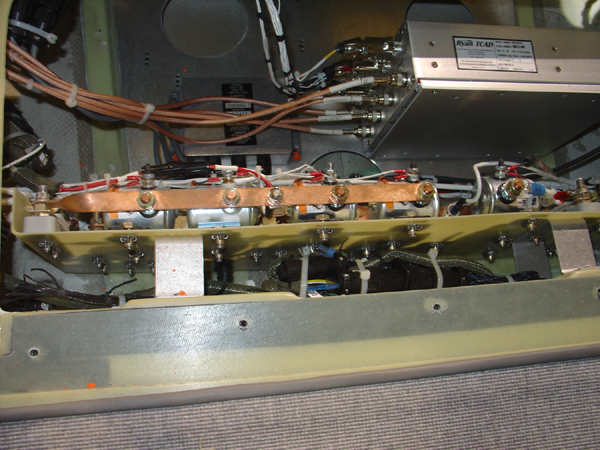

Below is the weirdest picture you will ever see of a Lancair Columbia-400… the Traffic-detection system and maybe some other stuff as the plane is really opened up for repairs. Look at the perfect workmanship, beautiful metal, perfect strong fiberglass and fittings! 100 years of evolution clearly behind each component. OOOO! Me likee!

Summary:

OK, I sound a bit cocky in this adventure… SORRY! The facts are with me. I am saying it all in hopes that I can help others out.

Should you:

1: Have your Corvette or similar car modified? (YES, you should, if you want to amp-it-up! It will make your Vette truly fun, powerful, and unique!)

2: Buy insurance? (Well, you are CONSISTENTLY buying a nickel for a dime, over and over and over. And even THAT assumes that the insurance company actually PAYS OUT when it is needed, and if you believe that they always will, then I have a bridge to sell you. You could take the money that you WOULD have spent on insurance and INVEST it, so you MAKE money over time, rather than LOOSE it. That’s what I do. You will prolly get about a 10% annual GAIN in your money, rather than a 44% LOSS.

According to http://www.first-draft.com/2007/08/boxing-gloves-a.html :

At Allstate, claims paid fell from 87.2 percent of premiums charged in 1992 to 43.5 percent last year, according to the CFA’s Hunter.

At State Farm the ratio dropped from 77.5 percent in 1994 to 66.6 percent in 2005,

while at Farmers it fell from 74.7 percent in 2001 to 56.9 percent.

According to this, every dollar you pay into these companies gets you about 56 cents back. In other words, for an investment, buying insurance is voluntarily taking a 44% loss every year. Is that the type of investment return you want? I gain about 10% to 20% in the market each year with aggressive mutual funds. You want to lose 44% per year instead? Buying insurance, you are! Me wanting the best for you, I would say you might consider investing that money so it EARNS a return, rather than consistently LOSING it!

austin